The Council of Ministers recently issued an amendment (106/2024) (“Amendment”) to the Companies Law (1/2016) (“Companies Law”) with respect to the quorum and majority requirements of limited liability companies’ Extraordinary General Meetings (“EGM”). The Amendment could have significant effects on current business practices in Kuwait, and specifically on foreign shareholders in Kuwait. What is an EGM? An EGM is a general partners meeting that enables partners to pass significant decisions with respect to a company’s operations and dealings. Examples of such decisions include:

(1) Amending the company’s articles of incorporation;

(2) Resolving to merge, transform or spin-off the company;

(3) Increasing or decreasing the company’s capital;

(4) Dismissing or changing the company’s manager, or otherwise limiting his authorities, only if the manager is specified by name in the company’s articles of incorporation; or

(5) Dissolving the company. The competency of an EGM vis-à-vis a limited liability company’s operations and constitution is much higher than that of an Ordinary General Meeting (“OGM”), which is somewhat limited to ratifying business and financial reports and passing other ordinary decisions relating to the company’s operations. Status Quo Before the Amendment

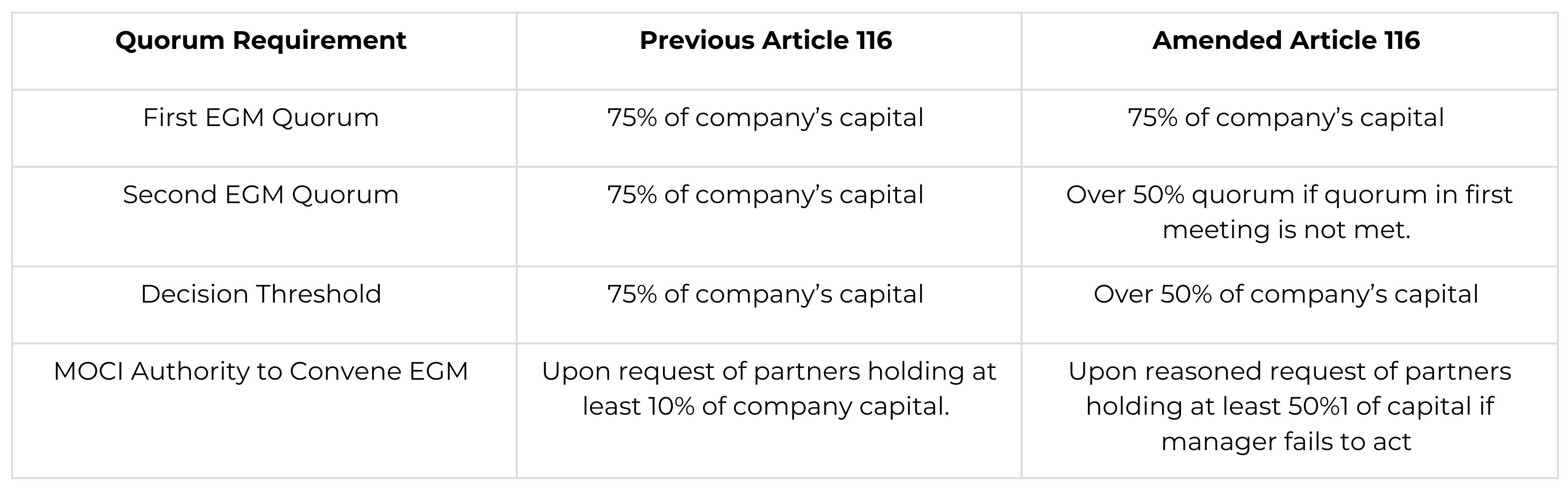

Prior to the Amendment, the Companies Law’s provision with respect to EGMs, Article 116, required that an EGM could only be valid if partners representing at least three-quarters (75%) of the company’s capital were present. Furthermore, resolutions could only be passed with the approval of partners holding at least three-quarters (75%) of the company’s capital. This higher threshold often created both advantages and challenges for convening EGMs and passing resolutions. On the positive side, requiring the attendance and approval of partners holding at least three-quarters (75%) of the company’s capital ensured that major decisions reflected a strong majority consensus. This high threshold acted as a safeguard against unilateral decision-making by a small group of partners, protecting the interests of minority shareholders. It provided stability in governance and prevented contentious or hasty decisions that might harm the company’s long-term viability. However, the drawbacks of such a stringent requirement became apparent in practice. The high quorum and majority threshold often created significant challenges in convening EGMs and passing resolutions, particularly in cases where achieving the required attendance or agreement among partners was difficult. Companies frequently faced delays in decision-making, as failing to meet the quorum meant that critical decisions could not be addressed, even in urgent situations. This was especially problematic for companies with fragmented ownership structures or absentee partners, such as those with foreign partners who may not be readily available to participate in meetings. Additionally, this structure sometimes led to deadlocks, where a minority of partners holding just over 25% of the capital could block resolutions, effectively stalling the company’s ability to respond to pressing operational or strategic needs. For example, efforts to remove a non-performing manager or approve necessary capital increases could be thwarted by a small minority, even if the majority supported the change. Post-Amendment

1- Quorum

In light of the Amendment, while the quorum for the first EGM remains unchanged (requiring the attendance of partners owning at least 75% of the company capital), the Amendment now introduces the possibility whereby in the event the quorum (at least 75%) is not met in the first EGM, a second EGM can be convened whereby a lower quorum is required: the attendance of partners owning more than half (50%+1) of the company’s capital. This adjustment provides the possibility of a second EGM with a lower quorum. 2- Majority Threshold

Another pivotal change introduced by the Amendment is the lowering of the decision-making threshold. Previously, EGM resolutions required the approval of partners holding at least 75% of the capital, making it difficult to pass resolutions even when the majority of partners were in agreement. Under the new rules, EGM resolutions can now be passed with a majority exceeding 50% of the company’s total capital, regardless of whether the meeting is the first or second EGM. Ministry of Commerce and Industry (“MOCI”) Involvement

Further, the Amendment increased the minimum capital ownership required by the partners to not less than half of the company capital (50% or more) should the partners wish for the MOCI to call for an EGM in the event the manager of the company fails to do so. Prior to the Amendment, partners owning at least 10% of the company capital were required for the manager to convene an EGM. Partners owning not less than 10% of the company capital would request for the MOCI to convene the EGM should the manager fail to do so. Pursuant to the Amendment, the percentage increased from 10% to 50% of capital ownership by the partners. Should the manager fail to convene an EGM, partners owning at least 50% can submit a reasoned request to MOCI for the latter to convene the EGM. The MOCI shall invite the partners to convene an EGM upon the submission of a reasoned request by the partners representing at least half of the company’s capital.

Our Thoughts

The amendment reducing the quorum to more than 50% in the second EGM increases the chances of convening EGMs and this may be helpful in cases where a resolution is needed for the viability of a company, i.e., where partners wish to remove a poorly performing manager who was appointed in the company contract but were not able to remove him due to failure in obtaining a 75% quorum and majority requirement.

By reducing the majority threshold to more than 50%, the chances of issuing EGM resolutions have increased.

However, as the majority threshold was reduced to more than 50% instead of 75%, local partners have the upper hand in WLL structures given the 49% ceiling for foreign ownership of Kuwaiti companies under the Commercial Code. In such cases, the local partner can obtain resolutions without the need for the foreign partner’s attendance or vote. This dynamic shifts the balance of power in favor of local partners, leaving foreign partners at a disadvantage.

To address this concern, it may be possible to amend the majority threshold in the company contract pursuant to Article 113 and 115 of the Companies Law whereby a higher majority threshold for passing resolutions of EGMs can be included in the company contract.

It is notable to point out that even though the Companies Law stipulates such option, we may face some hurdles with MOCI when implementing it due to MOCI’s online portal not offering all options stipulated in the Companies Law.

In summary, while the Amendment facilitates more efficient governance and decision-making, careful structuring of partnership agreements is essential to balance the interests of all parties.

1 - Executive Summary & Core Conclusion The attached commentary critiques Kuwait’s Ministerial Resolution No. (351) of 2025. While nominally drafted to "regulate" the commercialization of energy drinks, the resolution effectively functions as a de facto prohibition by severely restricting viable distribution channels. From an administrative law perspective, the decree… Read more

In light of recent regional developments and heightened market volatility across the GCC, regulatory authorities have taken precautionary measures to safeguard market stability and investor confidence. These measures reflect a proactive approach aimed at managing systemic risk, preserving orderly trading conditions, and mitigating the impact of short-term uncertainty on capital… Read more

Overview In a significant step to strengthen and modernize Kuwait’s collective investment schemes framework, the Kuwait Capital Markets Authority (the “CMA”) has introduced a new wave of reforms under Decision No. (18) of 2026 (the “Decision”), issued on 12 February 2026. The Decision establishes a dedicated regulatory framework for multi-asset… Read more

Overview The UAE has issued a new Civil Transactions Law (Federal Decree-Law No. 25 of 2025), which will enter into force on 1 June 2026 and replace the 1985 Civil Code. While the new law preserves the UAE’s civil law and Sharia-based foundations, it introduces clearer and more structured rules… Read more

Meysan advised on the successful establishment of the KWD 50 million Senior Unsecured Bonds Programme by Kuwait Financial Centre (Markaz) and the issuance of the First Tranche of Bonds with value of KWD 35 million. The First Tranche of the Senior Unsecured Bonds Programme was successfully issued to qualified investors… Read more

In a significant development for Kuwait’s capital markets, the Capital Markets Authority (“CMA”) and BoursaKuwait have recently introduced new regulatory reforms intended to widen market access and support the growth of emerging ventures. On 29 June 2025, the CMA issued Decision No. 108 of 2025 (the “CMA Decision”), introducing the regulatory… Read more